When your vehicle is declared a total loss after an accident, theft, flood, fire, or another covered event, the settlement process can feel confusing fast. Many policyholders hear the phrase USAA total loss protection and assume it works the same way as GAP insurance or new car replacement coverage. In reality, USAA's main total loss enhancement is its Car Replacement Assistance, often called CRA.

USAA Car Replacement Assistance is optional coverage that pays 20% more than your vehicle's actual cash value if your car is totaled or stolen. That extra amount can help you replace your vehicle, reduce an out-of-pocket loan balance, or give you more flexibility after a loss. It is not the same as traditional GAP insurance, which is designed specifically to cover the difference between your vehicle's value and your remaining loan balance.

Below is what policyholders should know about USAA total loss protection, how USAA total loss settlement offers are calculated, and what you can do if the settlement amount seems too low.

Understanding USAA Total Loss Protection.

The phrase USAA total loss protection is commonly used to describe the financial protection available when a USAA-insured vehicle is declared a total loss. In most cases, this protection comes from your standard auto policy, plus any optional endorsements you purchased.

For a typical total loss claim, USAA pays the vehicle's actual cash value, or ACV, minus your deductible. Actual cash value generally means the market value of the vehicle immediately before the loss, considering factors such as age, mileage, trim, options, condition, accident history, and comparable vehicle sales in your area.

If you purchased Car Replacement Assistance, your settlement may include an additional 20% of the vehicle's ACV. This is the key feature that separates CRA from a standard USAA total loss payout.

What Is USAA Car Replacement Assistance?

USAA Car Replacement Assistance is an optional auto insurance coverage that increases your payout if your covered vehicle is totaled or stolen. Instead of receiving only the vehicle's ACV, qualifying policyholders receive 20% more than the vehicle's actual cash value. USAA states that the money can be used however you want, whether or not you have an auto loan.

For example, if USAA determines your vehicle's ACV is $25,000, Car Replacement Assistance could add another $5,000 before any applicable policy terms, deductible handling, or lienholder payment considerations. That extra amount can make a major difference when replacement vehicles in your area cost more than expected.

CRA can be especially useful for:

- Newer vehicles that have depreciated quickly.

- Vehicles with higher replacement costs in the current market.

- Policyholders who want more than a standard ACV payout.

- Drivers who owe money on a loan but do not have traditional GAP coverage.

- Owners who want extra funds toward a replacement vehicle, even if the car is paid off.

Is USAA Total Loss Protection the Same as GAP Insurance?

No. USAA total loss protection through Car Replacement Assistance is not the same as traditional GAP insurance.

GAP insurance is designed to address a specific problem: owing more on a loan or lease than the vehicle is worth. If your car is totaled and your ACV settlement is lower than your loan balance, GAP coverage may help pay the difference.

Car Replacement Assistance works differently. It adds 20% to the vehicle's ACV after a covered total loss or theft, regardless of whether you have a loan. However, that 20% increase may or may not be enough to fully cover negative equity. USAA describes GAP insurance as coverage that pays the difference between what a vehicle is worth and what is owed on the loan, while CRA provides an added amount above the car's value instead.

This distinction matters. If you are upside-down on your loan and your USAA total loss settlement does not fully satisfy the balance, you could still be responsible for the remaining amount unless another coverage or loan product applies.

How USAA Determines a Total Loss.

A vehicle may be declared a total loss when it cannot be safely repaired or when the repair cost is too high compared to the vehicle's value. State law often plays a role in this decision because many states use total loss thresholds or total loss formulas. In general, insurers compare the cost to repair the vehicle, the vehicle's pre-loss value, and sometimes the salvage value to decide whether the car should be repaired or totaled.

Common factors that influence a total loss decision include:

- Estimated repair costs.

- Supplemental damage found after teardown.

- The vehicle's pre-accident ACV.

- State-specific total loss rules.

- Structural, frame, flood, fire, or safety-related damage.

- Salvage value.

- Parts availability and repair feasibility.

Once the vehicle is declared a total loss, the claim usually shifts from repair estimating to valuation.

How a USAA Total Loss Settlement Is Calculated.

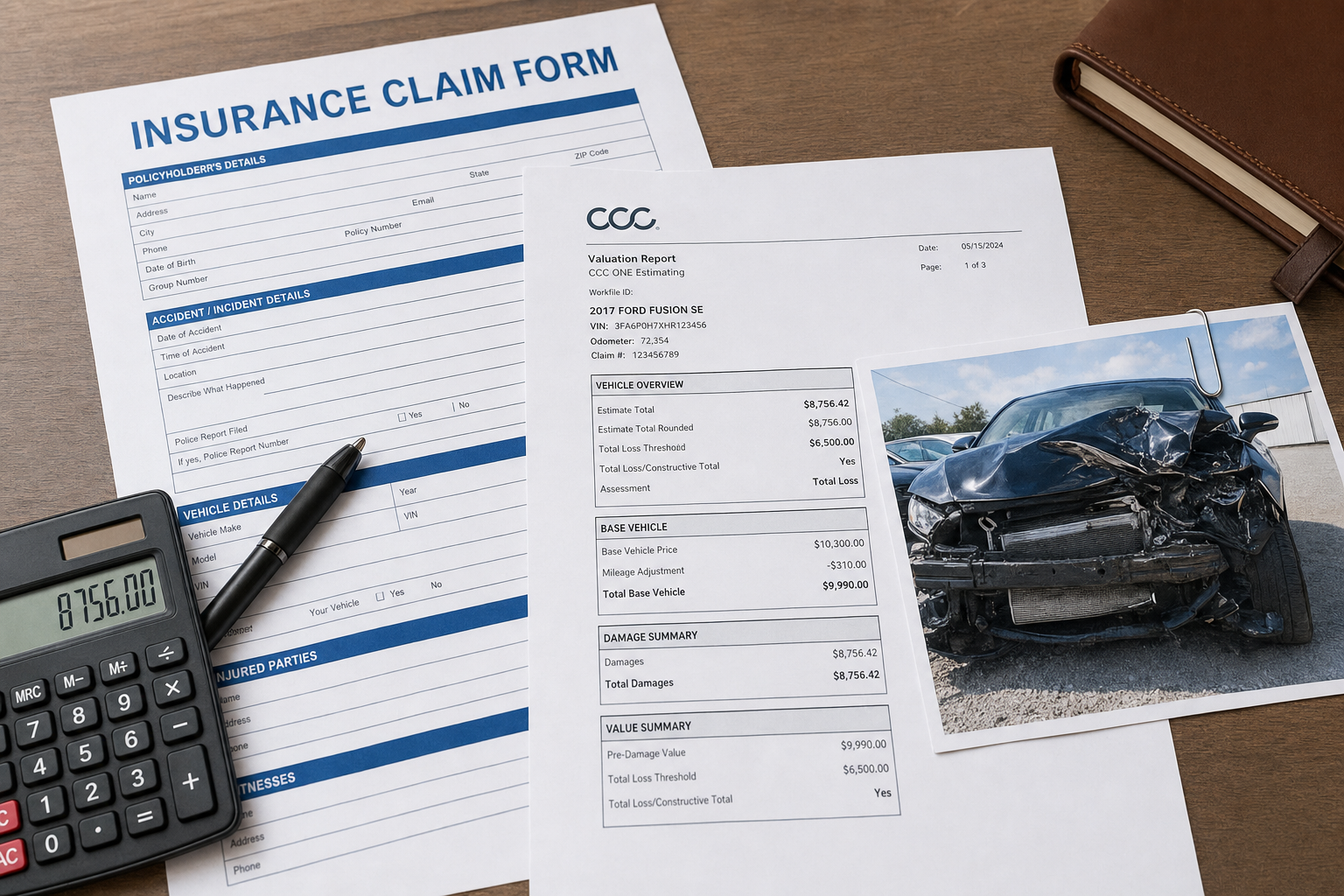

A USAA total loss settlement typically begins with a market valuation report. This report is used to estimate what your vehicle was worth immediately before the loss. The valuation should account for your vehicle's specific year, make, model, trim, mileage, options, condition, and local market data.

A standard USAA total loss settlement generally follows this formula:

Actual Cash Value – Deductible = Base Settlement

If you have Car Replacement Assistance, the settlement may include the additional CRA benefit:

Actual Cash Value + 20% CRA Benefit – Deductible = Enhanced Settlement

The exact payment flow depends on whether you own the vehicle outright or have a lienholder. If you have a loan, USAA may pay the lienholder first. Any remaining settlement amount is typically paid to you. If the settlement is not enough to pay off the loan, you may need to resolve the remaining balance unless another applicable product covers it. USAA notes that total loss claims may require documents such as a bill of sale, odometer statement, and certificate of title.

What Happens During the USAA Total Loss Claim Process?

While every claim is different, most USAA total loss claims follow a similar path.

- You Report the Claim — The process starts when you report the accident, theft, or covered loss. USAA assigns the claim, reviews coverage, and begins investigating the damage.

- The Vehicle Is Inspected — An adjuster or appraiser reviews the damage and repair estimate. If the repair costs are high enough, or if the vehicle cannot be safely repaired, USAA may declare the vehicle a total loss.

- USAA Prepares a Vehicle Valuation — USAA then determines the vehicle's ACV. This valuation should reflect the vehicle's pre-loss market value, not what you originally paid and not necessarily what it costs to buy a brand-new replacement.

- You Review the USAA Total Loss Settlement Offer — You should receive a valuation report or settlement breakdown. Review it carefully before accepting. Errors in trim, mileage, options, condition, packages, comparable vehicles, or local market adjustments can reduce your payout.

- Title, Lienholder, and Payment Issues Are Handled — If there is a loan, the lender is typically paid first. If the vehicle is paid off, payment generally goes directly to you. You may also need to provide title documents, an odometer statement, and other required paperwork.

- CRA Is Applied if You Purchased It — If your policy includes Car Replacement Assistance and the claim qualifies, the 20% CRA benefit should be included in the settlement calculation. Always review your declarations page or ask USAA to confirm whether CRA applies.

Why Your USAA Total Loss Settlement May Seem Lower Than Expected.

Many policyholders are surprised when the first USAA total loss settlement offer is lower than the price of similar replacement vehicles online. This can happen for several reasons.

The valuation may be based on adjusted comparable vehicles instead of the exact listings you are seeing. The report may also include condition deductions, mileage adjustments, prior damage deductions, or missing options. In some cases, the comparable vehicles may not match your trim, drivetrain, packages, or local market.

Common valuation issues include:

- Incorrect trim level or submodel.

- Missing factory options or packages.

- Incorrect mileage.

- Undervalued vehicle condition.

- Comparables from outside your true market area.

- Dealer listings adjusted downward without clear support.

- Prior damage deductions that are too aggressive.

- Failure to account for recent maintenance or upgrades that affect value.

- Comparable vehicles that are not actually available for purchase.

You do not have to assume the first number is correct. A total loss settlement is a valuation opinion, and valuation opinions can be challenged with the right evidence.

Tips to Increase Your USAA Total Loss Settlement Offer.

If your USAA total loss settlement offer seems too low, take a careful and organized approach before accepting payment. The goal is not simply to ask for more money. The goal is to show why the valuation does not accurately reflect your vehicle's pre-loss market value.

Review the Valuation Report Line by Line.

Start by checking the basic vehicle information. Confirm the VIN, year, make, model, trim, engine, drivetrain, mileage, packages, and options. Even small errors can change the value.

Compare the Listed Comparable Vehicles.

Look at the comparable vehicles used in the report. Ask whether they are truly similar to your vehicle. A lower trim, higher-mileage vehicle, former rental, accident-history vehicle, or out-of-market listing may not be a fair comparison.

Gather Your Own Market Evidence.

Find comparable vehicles for sale in your area that match your vehicle as closely as possible. Focus on the same year, make, model, trim, mileage range, drivetrain, and options. Save screenshots or PDFs of the listings because online listings can disappear.

Document Your Vehicle's Condition.

Provide photos, maintenance records, service history, tire receipts, recent repairs, and any documentation showing your vehicle was in above-average condition before the loss. A well-maintained vehicle may deserve a stronger condition rating than a generic valuation assumes.

Identify Missing Options and Packages.

Factory packages can significantly affect value. Examples may include technology packages, premium wheels, towing packages, upgraded audio, panoramic roofs, leather interior, advanced safety features, off-road packages, and performance packages.

Ask for Explanation of Deductions.

If the settlement includes deductions for condition, prior damage, mileage, or market adjustments, ask for a clear explanation. Unsupported or excessive deductions may be negotiable.

Confirm Whether CRA Applies.

If you purchased Car Replacement Assistance, make sure the 20% benefit is included. Do not assume it was automatically applied correctly. Ask for the settlement breakdown in writing.

Consider an Independent Appraisal.

An independent auto appraisal can provide a professional, unbiased valuation that challenges an inaccurate insurance valuation. This can be especially useful when the settlement is thousands of dollars below comparable market listings.

What If You Owe More Than the Vehicle Is Worth?

If you owe more than the vehicle's ACV, your loan does not automatically disappear. USAA's standard total loss payment is based on the vehicle's value, not your loan balance. If you have CRA, the extra 20% may help reduce or eliminate the shortfall, but it is not guaranteed to cover all negative equity.

For example, if your vehicle's ACV is $20,000 and your loan balance is $26,000, a standard settlement may leave a significant balance after the lender is paid. CRA could add $4,000 in this example, but you may still owe the remaining difference depending on your deductible, loan balance, and policy terms.

This is why it is important to understand your coverage before a loss occurs and to review your settlement carefully after a total loss.

Why an Independent Appraisal Can Help With a USAA Total Loss Settlement.

Insurance company valuations are not always wrong, but they are not always complete either. A strong independent appraisal can help identify valuation errors, unsupported deductions, missing equipment, poor comparable selections, and market evidence that better reflects your vehicle's actual pre-loss value.

An independent appraisal may be helpful when:

- The settlement offer is lower than local replacement listings.

- The valuation report uses poor comparables.

- Your vehicle had rare options, packages, or upgrades.

- Your vehicle was in excellent condition.

- The insurer undervalued your trim or configuration.

- You need a professional report to support your counteroffer.

A detailed appraisal gives you evidence, not just an opinion. That evidence can strengthen your position when negotiating a fair USAA total loss settlement.

How Auto Claim Consultants Helps With USAA Total Loss Claims.

Auto Claim Consultants is a nationwide independent auto appraiser that provides unbiased vehicle valuations for total loss and diminished value claims. We specialize in detailed evaluations designed to help policyholders pursue fair compensation when an insurance settlement does not accurately reflect the vehicle's true market value.

Our team reviews the details that can make or break a total loss valuation, including comparable vehicles, mileage, condition, trim, options, packages, regional market trends, and insurer-applied deductions. Whether you are dealing with a standard USAA total loss settlement or a claim involving USAA total loss protection and Car Replacement Assistance, we can help you understand whether the offer is fair and what evidence may support a higher value.

Get Help With Your USAA Total Loss Settlement Today.

USAA total loss protection can provide valuable financial support after a vehicle is totaled, especially if your policy includes Car Replacement Assistance. CRA's 20% added benefit can make it easier to replace your vehicle or reduce the impact of a loan balance, but it does not guarantee that your settlement offer is accurate or that all negative equity will be covered.

Before accepting a USAA total loss settlement, review the valuation carefully, confirm your coverage, check the comparable vehicles, and gather evidence that supports your vehicle's true pre-loss value. If the offer seems too low, you have the right to question it.

For help with your USAA total loss claim, contact Auto Claim Consultants today. Our nationwide independent appraisal team can provide an unbiased vehicle valuation and help you pursue the fair compensation you deserve.

Disclaimer: Auto Claim Consultants provides independent appraisal and valuation support. We do not guarantee any specific settlement amount, claim result, or increase in value. Our opinions are based on available vehicle information, market data, and appraisal methodology.

FAQs.

What is USAA total loss protection?

USAA total loss protection generally refers to the coverage available when your vehicle is declared a total loss after a covered accident, theft, or other insured event. In most cases, USAA pays the vehicle's actual cash value, minus your deductible, unless you purchased optional coverage such as Car Replacement Assistance.

Is USAA total loss protection the same as GAP insurance?

No, USAA total loss protection through Car Replacement Assistance is not the same as traditional GAP insurance. CRA adds 20% to the vehicle's actual cash value, while GAP insurance is designed to cover the difference between your loan balance and the vehicle's value.

When does USAA declare a vehicle a total loss?

USAA may declare a vehicle a total loss when it cannot be safely repaired or when the repair cost is too high compared to the vehicle's actual cash value. State total loss laws and formulas can also affect whether a vehicle is totaled.

Who can help me dispute a USAA total loss settlement?

An independent auto appraiser can help you evaluate whether your USAA total loss settlement is fair. Auto Claim Consultants provides unbiased vehicle valuations for total loss and diminished value claims nationwide, helping policyholders pursue fair compensation.